One of of the key challenges faced by the Government today is increasing the ease of doing business in India that will provide impetus to self-employment and instill confidence among the investor community. Presumptive taxation is one such provision in the Income Tax Act. If you are a startup, micro or small enterprise

you might want to consider it.

Earlier presumptive tax applied only to businesses and professionals were specifically left out. But, not any more. Finance Bill 2016 extends it to professionals mentioned in section 44AA(1), including:

Earlier presumptive tax applied only to businesses and professionals were specifically left out. But, not any more. Finance Bill 2016 extends it to professionals mentioned in section 44AA(1), including:

- Legal

- Medical

- Engineering

- Architecture

- Accountancy

- Technical consultancy

- Interior decoration

- Notified profession

The amended section 44AD of the Income Tax Act applies

to resident individuals, HUFs or partnership firms (except LLP) running a

business and having turnover of Rs. 2 cr or less. The business of plying, hiring or leasing goods carriages is separately covered u/s 44AE. Units claiming exemption under certain other provisions of the Income Tax Act are also excluded. Section 44AD does not impose a mandatory condition, rather it offers an option, where an entity can claim 8% of the turnover as its taxable

income for the year. For example, if the turnover is Rs. 50 lac the taxable income will

be deemed to be Rs. 4 lac. The assessee can voluntarily disclose a higher income.

Similar to above, the newly introduced section 44ADA applies to

professionals with gross receipts of Rs. 50 lac or less. The presumptive income

will be equal to or higher than 50% of the gross receipts. All other inclusions and exclusions are same as above.

Presumptive taxation serves two main purposes. On the side of the Exchequer, it increases tax compliance and on the side of the taxpayer it significantly simplifies compliance. No books of accounts need to be maintained u/s 44AA and the requirements of tax audit u/s 44AB will not apply. Since the calculation of the notional taxable income is straightforward, possibility of litigation is minimized. The assessee has an option to declare higher taxable income, but it is not an obligation. Therefore, the Assessing Officer cannot impose a higher tax liability. However, it is a prudent approach to seek expert guidance and understanding the full impact of the provisions of this valuable option.

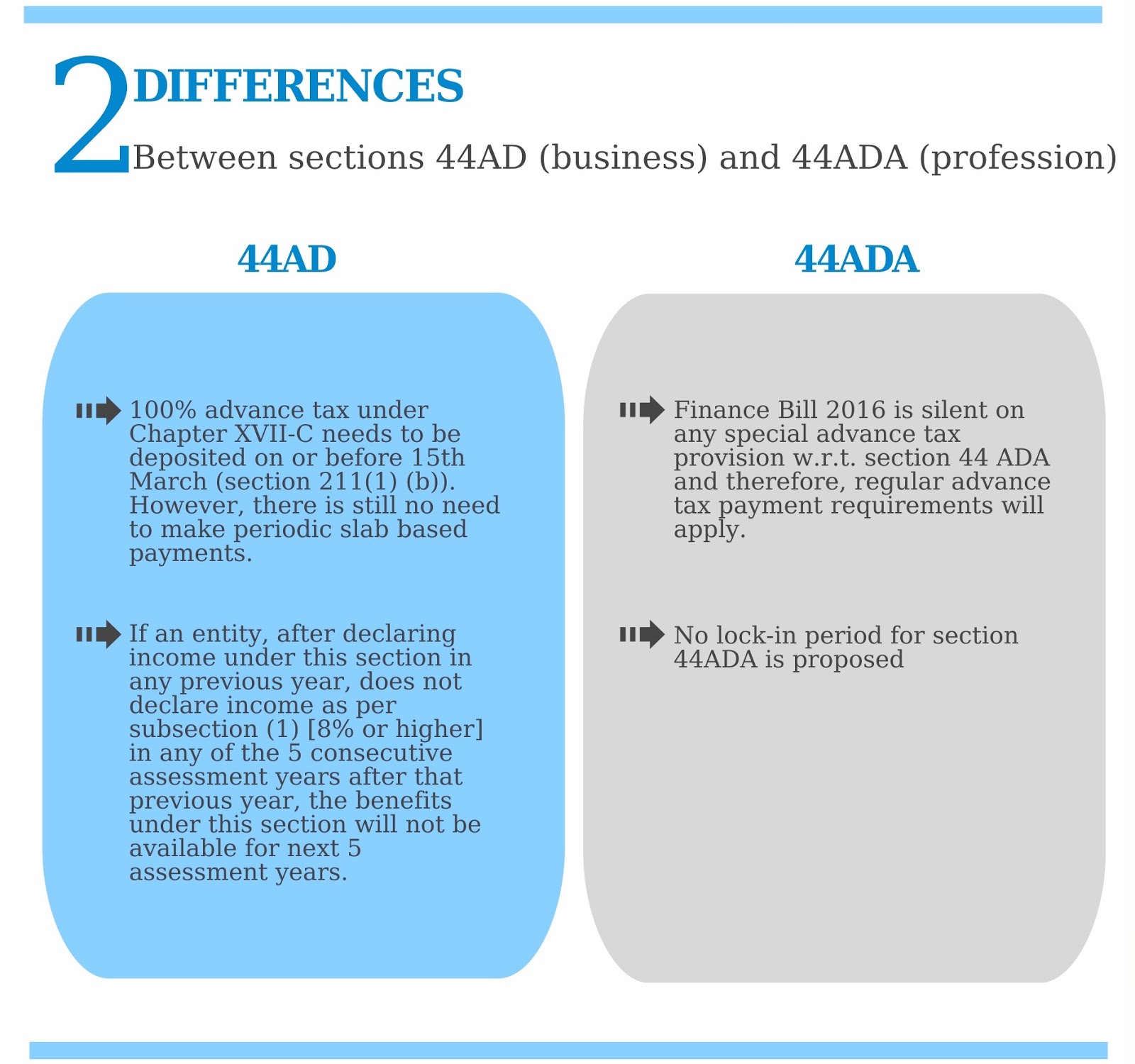

Budget 2016 has brought 3 amendments to section 44AD. Firstly, the Bill has omitted the proviso to

section 44AD (2), which allowed additional expenses on account of interest and

remuneration paid to partners u/s 40(b). Secondly, advance tax provisions will not apply u/s 211(1)(b). Under the amended section, 100% advance tax

under Chapter XVII-C needs to be deposited on or before 15th March. Thirdly, a 5 year lock-in period is proposed. Accordingly, if an entity, after declaring income under this section in a previous year, does not do so as per subsection (1) [8% or higher] in any of the 5 succeeding consecutive

assessment years, the benefits under this section will not be available for

next 5 assessment years.

Eurion Constellation helps startups and MSMEs in India in establishing and expanding their presence. Areas from business planning & statutory compliance to fund raising & restructuring are covered by us under one roof. Contact us for more details. Follow us on Twitter and Facebook for regular updates.